A Better Way to Think About Retirement Provision

Introduction

Retirement provision has long been a significant part of national economic policy. The social contract in modern societies carries a clear promise that if individuals participate in economic life and contribute through work and taxation, they will not be abandoned in old age, instead enjoying the benefits of a decent standard of living.

A society must organise itself so that those currently producing goods and services generate a surplus beyond their own consumption, sufficient to sustain those who are no longer working. However complex the institutional design for achieving this result, the requirement for it is universal and is a central theme of this essay.

This immediately makes pensions a collective macroeconomic issue rather than a matter of individual financial planning. At any point in time, the goods and services consumed by retirees must be produced by those who are currently working. No arrangement of savings accounts, pension funds, or financial portfolios alters this fact. What differs between pension systems is not whether today’s workers support today’s retirees, but how that transfer of real resources is organised and distributed.

Yet much contemporary discourse around pensions obscures this reality. Public debate tends to frame pensions through the language of fiscal affordability, individual prudence, or the sustainability of government budgets, particularly in relation to policies such as the triple lock. We are asked whether the state can ‘afford’ future pensions, whether households are saving enough, or whether demographic change renders existing commitments untenable. These questions are typically posed as though the constraint were financial, rather than rooted in the organisation of real economic activity.

Closely related to this is the widespread focus on demographic metrics such as the Old Age Dependency Ratio (OADR). As society ages and becomes increasingly in poorer health, a change in the ratio of workers to retirees is clearly relevant to how we provision retirement. But a growing dependency ratio is frequently treated as a deterministic indicator of crisis, rather than as a high-level constraint input into a broader question about how societies adapt their patterns of production, distribution, and care. A higher dependency ratio does not automatically imply unsustainability, it implies that choices must be made about what is produced, who produces it, and how the resulting output is shared.

Economies do not exist to maximise financial balances or accounting aggregates. They exist to provision people with the goods and services required for a dignified life across all stages of that life in a sustainable way. Designing an economy capable of supporting an ageing population is therefore not a question of finding the money or restraining public spending due to perceived ‘unsustainable’ future public liabilities. It is a question of ensuring that sufficient real resources are available at the time they are required, and that institutional arrangements distribute access to those resources in a way that is socially coherent and politically legitimate.

This essay argues that much confusion surrounding pensions and fiscal sustainability arises from a persistent mis-framing of the problem. By analysing retirement provision through a real resource flow lens, and by re-centring the discussion on real production and distribution rather than financial abstractions, it becomes possible to see more clearly what the genuine challenges and policy questions that actually need addressing are. Only with this clearer macroeconomic framing can sensible and durable policy choices be made about how we provision old-age consumption, both in the UK and more broadly.

The UK Pension Model

The UK has a unique pension mix compared to other advanced economies, one that relies more on individual saving and private wealth (like workplace pension schemes and property) and less on the state. This mix reflects decades of policy choices about who should bear the distributional cost of supporting an ageing population, and how this is best achieved.

By design, the UK entrusts a large share of retirement income to private provisions while the state pension primarily serves as a basic floor. Workplace pension schemes, personal financial assets, and housing wealth therefore constitute the bulk of wealth stocks owned at the point of retirement. This institutional choice becomes clear in international comparison where British retirees receive just over 22% of average earnings from the state pension, the lowest share in the G7, compared with 58% in France and 76% in Italy.

In those systems, public pensions provide the majority of retirement income, often exceeding 70% of total pensioner income. In the UK, the equivalent figure is closer to 40% on average, reflecting a deliberate shift toward private saving (Money Week, 2025). The UK correspondingly devotes a smaller share of GDP to state pensions and age-related benefits than most advanced economies (House of Commons Library, 2024). Lower public spending and lower contribution rates are therefore features of a model that places greater responsibility on individuals to accumulate private wealth over their working lives.

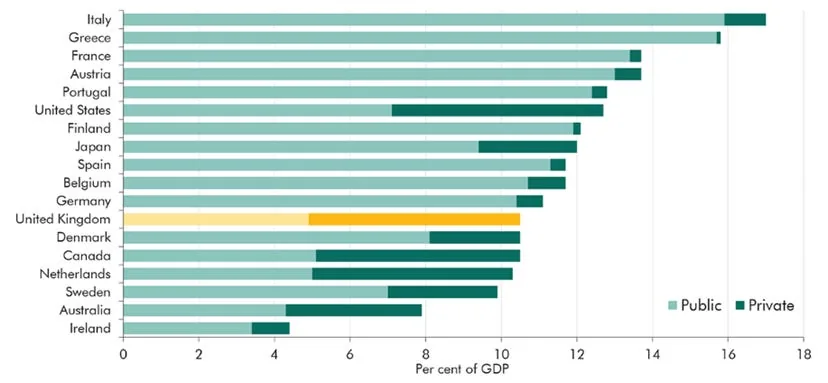

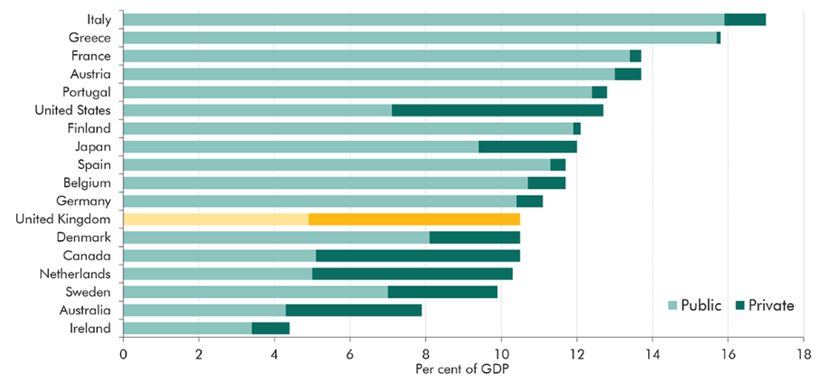

Figure 1 shows public and private pension benefit spending in 18 OECD countries for 2019. At a combined total pension spending of just over 10% of GDP, the UK is situated in the middle of the table. However, the composition differs markedly as more than half of UK pension income derives from private schemes rather than public transfers. Only Australia and Ireland in this group devoted a smaller share of national income to public pension provision in 2019.

Figure 1 - Public and private pension benefit spending in OECD countries, 2019. Source: OBR, OECD (OBR, 2025).

The state pension provides a relatively modest, flat-rate income floor. For a full national insurance tax contribution record it is currently just over £200 per week, rising to around £240 pw or ~£12500 per year from April 2026 (IFS, 2025). Public pension replacement rates in the UK are among the smallest in the OECD, meaning the state assumes only a limited role in maintaining pre-retirement living standards.

In the UK, this income gap is expected to be filled via private saving throughout a working life. Automatic enrolment has expanded workplace pension scheme coverage across the workforce. As a result, a large share of retirement income is tied to accumulated financial assets and the performance of capital markets rather than guaranteed public transfers.

Housing wealth forms a significant additional source of consumption in this more privatised model. Culturally and financially, many people view owning a home (or a second property) as a key way to support themselves later in life. In aggregate, housing wealth now exceeds pension wealth and for many households, owner-occupation is implicitly treated as a retirement strategy, whether through downsizing, renting out property, or equity release. This reliance on asset appreciation as a route to old-age security is much less pronounced in countries with more generous public systems and this structural reliance on property wealth explains in part the excessive demand for housing the UK has observed, driving up prices and rents across the board.

One consequence of this private pension model is not simply diversity of income sources but greater wealth and income inequality. Those with strong lifetime earnings and access to compounding asset markets can accumulate substantial private wealth, often driven less by productive effort and more by asset price inflation over recent decades. Those without such advantages rely primarily on the state pension, which provides subsistence rather than comfort and retirement outcomes therefore track lifetime income and asset ownership far more closely in the UK than in systems where public pensions dominate.

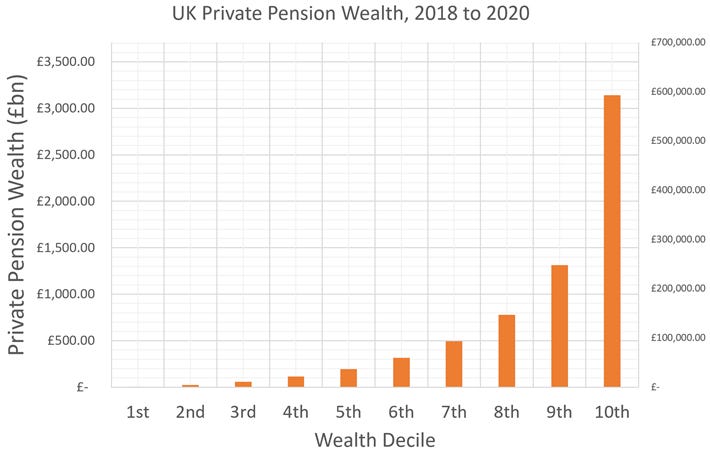

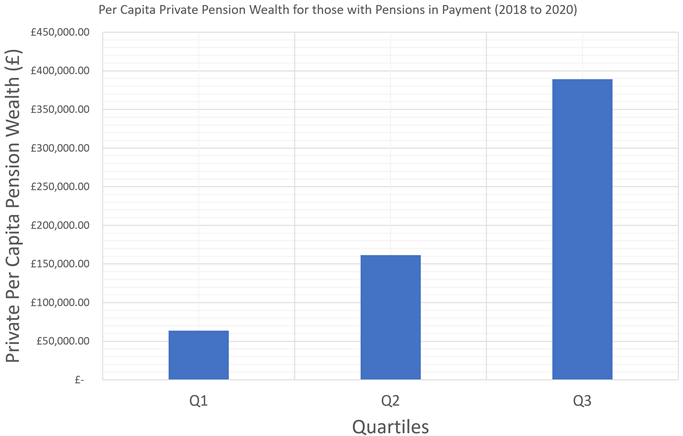

Figure 2 illustrates the distribution of UK private pension wealth across deciles between 2018 and 2020 for all age cohorts. Pension wealth in the top decile exceeded 600 times that of the lowest decile. Figure 3 presents similar data for those already in receipt of pension income, predominantly individuals aged 50 and above, of which 77% are above state pension age. It is clear that private pension wealth and the income derived from it are distributed very unevenly. However, this should not come as a surprise to anyone who understands the course of wealth inequality overall over the past half century. Furthermore, these figures likely understate concentration further, as inequality within the top decile and percentile is not fully captured.

Figure 2 - UK private pension wealth by decile, 2018 to 2020. (ONS, 2025); Author’s own plot.

Figure 3 - Private pension wealth distribution between 2018 to 2020 of those with pensions already in payment (ages ~50+) (ONS, 2025); Author’s own plot.

Nevertheless, a consistent thread throughout this essay is to always step back and regain a macro perspective. Whether retirement income comes from public transfer, via dividends and gilt coupon payments, or via rental income, returns on private capital, or house sales, the underlying reality is the same: retirees consume goods and services produced by the current workforce. The UK model does not get around this real economic requirement, but it does alter who holds the financial claims and how the transfer is mediated. Greater public understanding of this truth is a useful first step in developing sustainable retirement provision in real terms.

The Fallacy of ‘Funded’ Retirement

The state pension in the UK is linked to qualifying years of national insurance tax payments but it’s fundamentally a current government transfer financed through public spending. In a defined benefit scheme, retirees receive an income linked to their previous salary and years of service, typically underwritten by employers and ultimately dependent on their ongoing solvency. In the now dominant defined contribution model, individuals accumulate financial assets during working life which they later draw down in retirement.

However, to repeat my central argument, no matter how pensions are organised, retirees consume output produced by those currently working. If you are not working (and most retirees are not), yet you still need food, energy, healthcare, and other goods or services, those must be provided, in part, by someone else’s labour. This is an inherent inter-generational transfer whereby resources flow from the working population to the non-working population. No matter how much financial wealth retired people have saved, when they are retired, they live entirely off of the real production of the younger generation. If you are not producing anything, but you are still consuming, you are by definition benefiting from the surplus production of others whether you hold an accumulated stock of financial wealth or not.

To be clear, this observation is not a moral critique. Intergenerational transfer is not a flaw in the system but a defining feature of any functioning society. The social contract depends on it. Without the expectation that working generations will support those who are no longer able to work, social cohesion would quickly erode. While some may resent the idea that part of their production surplus sustains retirees, the alternative would be to organise society on the principle that individuals may only consume what they directly produce. That is neither desirable nor reflective of how modern economies actually operate because in highly complex and advanced economies, many workers already consume more than their immediate labour input would imply. This is because output is generated by complex capital structures and essentials such as food provisioned by a relatively small number of people. Gone are the days of agrarian societies producing the food and consumption goods directly.

Imagine two societies with identical economies. In one, retirees have no savings and rely purely on a state pension provisioned by taxing current workers such that their own consumption is lowered commensurately. In the other, retirees accumulated a large stock of unspent income which they now spend to consume. In both cases, if retirees consume 10% of the nation’s goods and services, then 10% of current output is being devoted to the older generation. It doesn’t really matter whether that transfer happens via government budget or via private spending of accumulated funds. The real cost to society is the same.

Moreover, consider a defined contribution pension. During working life, individuals defer consumption, spend less than their labour income, and use the saving to purchase financial assets. Those assets represent claims on future income streams. When retirement arrives, assets are sold or income is drawn in order to consume. In aggregate, however, the assets being purchased by current savers are being sold by those currently dissaving, including existing retirees. Later, when today’s savers retire, they will sell to the next cohort. At any point in time, retirees as a group convert financial claims into consumption by exchanging them for the income and therefore surplus production generated by the current workforce.

Understanding this helps cut through a lot of political rhetoric. When it is claimed that “we can’t afford state pensions for all these retirees” we should ask “would we magically afford it if we instead force individuals to save more for retirement instead?” The total demand on the economy’s resources coming from retirees would not shrink just because the financial mechanism changed. If anything, reducing public pensions might just push the cost elsewhere: onto families (supporting elderly relatives), onto individuals (working longer or drawing down personal wealth), or onto the retirees themselves if they end up consuming less and suffering lower living standards.

This is where fallacies of composition frequently arise. At the individual level, saving more appears to ‘fund’ one’s retirement. At the macro level, however, saving does not create future goods and services by itself. It merely establishes a claim on whatever real production exists at that future point. The ability of retirees to enjoy a decent standard of living therefore depends not on the size of pension pots in isolation, but on the productive capacity of the economy at the time those pots are drawn down.

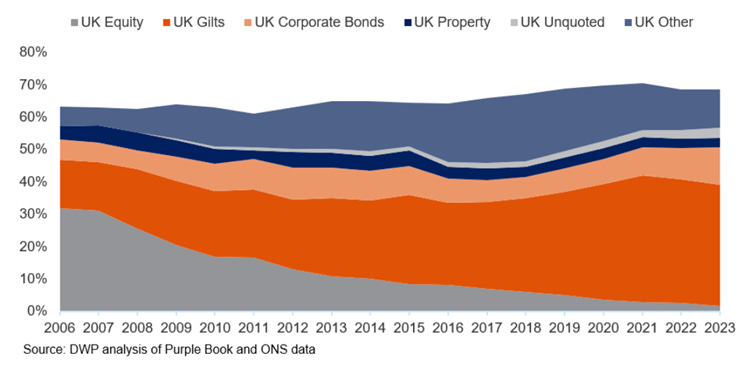

An additional layer complicates the UK case. A substantial proportion of defined benefit pension fund portfolios is invested in UK government liabilities, particularly gilts across a range of maturities. Figure 4 shows the composition of asset holdings for defined benefit pension funds, reflecting a significant shift into safer UK gilt holdings as these funds increasingly require liquidity and low risk holdings to make payments due (UK Gov, 2024). Notably, defined contribution schemes hold a far smaller proportion of their assets under management in UK gilts (4%) and UK equities more generally (30%), likely reflecting the relative differences between cohorts in each type of scheme and therefore current risk appetite.

Figure 4 – Composition of UK defined benefit pension asset holdings. White reflects overseas investments. UK gilt holdings comprise 37% of total asset stocks. (UK Gov, 2024)

In effect, a significant share of so-called private retirement provision consists of claims on future public interest payments. These assets do not, in themselves, finance new productive investment. They represent risk-free income streams paid by the state to sterling savers. The interest flows accrue in proportion to financial wealth and therefore reinforce existing inequality. In this sense, a large component of private pension income is directly state-financed but distributed regressively according to prior asset accumulation rather than according to social need. The distinction between ‘public’ and ‘private’ provision therefore becomes more blurred than political narratives often suggest.

The core issue is therefore not financial sustainability but real provisioning capacity and distribution. The next section looks at how demographic change affects that capacity, and what it implies for how output must be organised and distributed across society.

Financial Affordability is Always the Wrong Question

As noted, a frequent refrain in media and politics is that programs like the state pension are ‘unsustainable’ or ‘unaffordable’ as the number of retirees rises. We hear metaphors of the government budget being like a household that must tighten its belt.

But unlike a household, a currency-issuing government does not actually face a hard financial constraint in its own currency. It cannot ‘go broke’ in pound sterling because it can always afford to purchase anything for sale in its own currency at current prices or meet any nominal obligation denominated in that same unit. This was famously acknowledged by former US Federal Reserve Chairman Alan Greenspan when questioned about the solvency of US Social Security. He explained that

“..there’s nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The question is, how do you set up a system which assures that the real assets are created which those benefits are employed to purchase… it’s a question of the structure of a financial system which assures that the real resources are created for retirement.” – Alan Greenspan, Chairman of the US Federal Reserve 1987-2006(C-SPAN, 2005)

In short, money is never the binding constraint; real resources are. If the UK government tomorrow decided to double the state pension, it could make the payments without operational difficulty. The Bank of England and UK Treasury can always credit accounts; the challenge would be whether the economy could expand the supply of food, housing, healthcare, social care, energy, and leisure services without generating inflation or displacing other socially necessary production. If carers, hospital capacity, suitable housing, or resilient food systems are lacking, then higher nominal spending would bid up prices. The system would not have run out of money, it would have run out of real capacity (Wray & Nersisyan, 2023).

To be clear, this isn’t a call for ‘irresponsible’ fiscal spending. It’s about correctly identifying the problem and the real constraints we face. Over the long term, an ageing society might indeed face tough choices, but they are choices about real factors and should always be framed as such.

The OADR is rising and by mid-century roughly a quarter of the UK population will be over 65 (up from ~20% today) (ONS, 2019). Fewer workers relative to retirees means that each worker must, on average, produce a larger surplus over their own consumption if living standards are to be maintained.

However, some caution is needed as shifts in age-related economic activity over time have led to more pensioners working, at least in part time roles. This wider Active Dependency Ratio (ADR) measure is growing more slowly and may help to offset the impact of population ageing on the challenges of retirement provision in the future. Although, to what extent we want a society where many older people feel like they have little choice but to continue working later and later in life is a political economy and philosophical question.

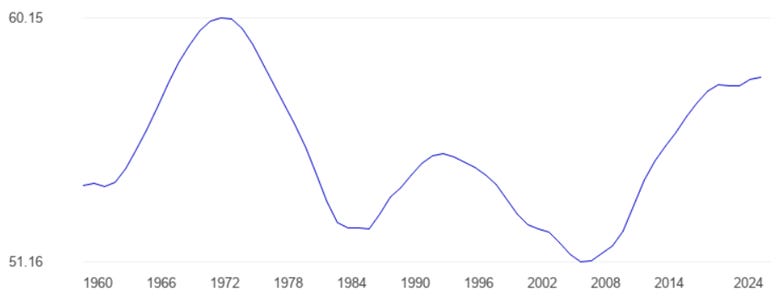

Historically, the UK has coped with similarly high total dependency ratios during the post-war baby boom, when a large child population was supported by a relatively smaller workforce. But societies adapt through changes in labour force participation, productivity, migration, and social organisation. Figure 5 depicts this total age dependency ratio for the UK from 1960 to 2024. A peak of 60% occurred in the early 1970s as demographics post-war shifted over time.

Figure 5 - Age Dependency Ratio (%) for the UK 1960 to 2024. Defined as the number of dependents younger than 15 and older than 64 as a proportion of the working age population (The Global Economy.com, 2024), World Bank Data.

Future dependency ratios in the UK, while predicted to be higher, are therefore not without historical precedent, albeit young dependents naturally age into an active workforce whereas older cohorts don’t. But moderate increases in productivity can offset a lot of the strain; for instance, if each worker can produce 20% more of the kind of output that is socially useful in the future while ensuring hard ecological limits are respected, having somewhat fewer workers can still suffice to maintain living standards and well-being for all.

Certain kinds of conspicuous or damaging consumption will likely have to be curtailed in the future and the capital structure we develop must reflect these strategic choices around what we choose to produce and consume. But there is nothing inherent preventing sufficiency and high-quality lives being led by all.

Aggregate real GDP tells us little about whether an economy is provisioning appropriately for an ageing population. It is neither a sufficient nor a necessary condition for satisfactory retirement provision. It is not sufficient because GDP growth tells us nothing about the composition of output. And it is not necessary because what matters is that the level and structure of production are adequate to meet the combined needs of workers and retirees within ecological limits. A stable or even contracting aggregate economy could, in principle, sustain dignified retirement if resources are reallocated appropriately and if socially necessary sectors are prioritised.

It is clear from this that production is heterogeneous. Social care, healthcare, energy infrastructure, food systems, and housing are not interchangeable with advertising services, premium entertainment subscriptions, or high-frequency trading. An economy can grow in aggregate while failing to expand the specific sectors that matter for old-age, wider wellbeing, and ecological sustainability.

Yet much political economy discourse assumes that if aggregate GDP is rising and markets are allocating resources through the price mechanism, then outcomes must be optimal. This assumption is fundamentally unwarranted and should be rejected. In the highly unequal and financialised capitalist economy we have, production will orient towards those with the strongest income streams and wealth positions, not necessarily toward those with the greatest social requirement.

If asset-rich older households command large dividend, interest, and rental flows, production will follow those preferences. If poorer retirees rely solely on a modest state pension, market allocation alone will not guarantee adequate provision of care, housing, or nutrition.

This is the real sustainability question we must tackle. Can the UK economy organise its productive capacity so that a growing older population has access to the goods and services required for a dignified life, without breaching ecological limits or undermining the living standards of younger generations?

Answering that question requires confronting structural choices. Should the retirement age gradually rise in line with healthy life expectancy? Should we invest in preventative healthcare to compress morbidity? Should AI, automation and productivity gains be directed toward socially necessary sectors rather than asset speculation? Should immigration policy be calibrated in part around demographic balance? And should credit and capital be steered away from property inflation and toward housing supply?

These are structural political questions with no clear-cut answers. They concern how labour, capital, and natural resources are deployed and it’s my view that answers to these questions should, to the maximum degree possible, be adjudicated in a democratically transparent way rather than allowing whatever is profitable to capital to direct our production systems.

Framing the issue primarily as a budget constraint distracts from these structural challenges and mires public discourse in irrelevant debates. Cutting state pensions does not create carers; expanding private pension saving does not build hospitals; austerity does not generate housing stock; and financial rearrangements do not, in themselves, expand the real capacity of the economy to support those who are no longer working. Economic organisation for the future requires far more than allowing market forces and whatever is profitable to capital to dominate. Market forces alone are unlikely to meet the structural challenges an ageing and ecologically constrained economy presents.

The Macroeconomics of Private Retirement Provision

It is worth examining the mechanics of how private pensions or property-based retirements work. Understanding this can illuminate whether the UK’s heavy reliance on private saving is economically efficient and justified.

Private Pension Funds

When you contribute to a pension during your working life, those contributions represent part of your saving. That unspent income is transferred into large institutional investment funds and used to purchase financial assets, typically a mix of equities, corporate bonds, government securities, and property-linked vehicles. The hope is that by the time you retire, these investment savings yield returns (dividends, interest, or capital gains) that you can use to consume. Importantly, what does it mean to cash out those investments in retirement? It means you are selling assets to or receiving payouts from corporations, governments, or other actors that are generating income in that future period.

If a pension fund holds government bonds, the income paid to the retiree comes from government expenditure in the future period. If it holds equities, the income derives from corporate profits generated by workers and consumers at that time. If assets are sold, they are sold to other savers, typically younger cohorts who are themselves deferring consumption. In every case, the retiree’s consumption depends on the productive capacity and income flows of the future economy. The financial instrument (be it a bond or stock) is a claim on future production.

The deeper presumption embedded in private pension optimism is that market allocation through the price mechanism will automatically guide savings into investments that expand precisely the forms of production required for future wellbeing. That presumption is contestable because firstly, we have known for many decades that saving flows do not finance investment flows at the macro level, the causality runs the other way.

Investment is not mechanically ‘financed’ by prior saving. In today’s monetary economies, investment decisions by firms and the state to expand physical and human capital generate income in the first instance. This then provides the income in excess of household consumption required for households and institutions to save. Therefore, the existence of large pension savings does not, by itself, cause productive investment to occur, it is merely the residual ex post outcome of non-consumption spending having taken place. But increasingly, this spending is not socially productive investment. Spending on speculative luxury property development, or environmentally destructive sectors can produce incomes and profits and therefore saving just as readily as spending on hospitals, renewable energy infrastructure, or social housing. From the perspective of national accounts, both generate income. But from the perspective of long-term retirement provisioning, they are not equivalent.

Furthermore, as discussed above, markets allocate purchasing power rather than social need. Profitability and existing wealth distributions determine where capital flows and demographic planning or ecological constraints play little role in firms’ investment decisions.

The smooth functioning of private retirement provision therefore depends not simply on growth, but on the structure of the economy that growth in desired areas produces, the sustainability of that structure, and the distribution of access to its output. These are political and institutional questions as much as economic ones.

Private funding can contribute positively where deferred consumption coincides with decisions to expand future productive capacity. If firms or the state choose to invest in new infrastructure, technology, housing, education, or other forms of socially useful capital, the future economy may be more capable of supplying the goods and services required by both workers and retirees. In that sense, retirement provision is made easier not because people saved, but because decisions were made to invest and build real capacity.

There also isn’t anything uniquely virtuous about private investment in this regard. The state can equally direct resources toward long-term productivity-enhancing and ecologically consistent investment through fiscal policy. The decisive factor is not whether investment is labelled private or public, nor whether it is preceded by saving. It is whether real resources are mobilised to expand socially necessary and sustainable productive capacity.

Property and Rent

Many households plan to finance retirement partly through housing wealth, whether by downsizing or by renting property. Selling a home in retirement transfers the asset to a younger buyer in exchange for financial claims that can be used to purchase current goods and services. The buyer, in turn, must either save or borrow to complete that transaction, constraining their own consumption or investment. If the retiree instead becomes a landlord, rental payments represent a sustained transfer from the tenant’s labour income to the asset holder. In both cases, housing wealth functions as a mechanism through which part of the working generation’s output is redirected toward retirees.

Reliance on property as a pension strategy can generate self-reinforcing dynamics. When housing is widely treated as a retirement vehicle, demand for property rises beyond its use as shelter and prices inflate, younger cohorts face higher barriers to ownership, and a larger share of wages is absorbed by rent or mortgage payments. Wealth inequality between asset holders and non-owners widens and in such a system, retirement security becomes increasingly tied to prior asset accumulation rather than to collective provision.

The broader point is that neither private pensions nor property-based strategies eliminate the fundamental economic task of supporting a retired population. They mediate that transfer differently but both inhabit the same macroeconomic flows. But some mechanisms are more unequal, more volatile, or more socially distortive than others and those without substantial private wealth remain reliant on public provision, which in the UK remains comparatively modest.

The fundamental nature of the problem is therefore best analysed across two levels.

-

The level, composition, and curation of real production output must align with the needs and binding constraints of society; and

-

The distribution and provision of this output must be equitable and aligned with long term social goals.

Putting the Triple Lock in Perspective

No discussion of UK pensions proceeds very far without encountering the triple lock. Since 2011 the state pension has been uprated each year by the highest of inflation, average earnings growth, or 2.5%. Its purpose was to prevent pensions from steadily falling behind living standards after decades in which price indexation eroded their relative value.

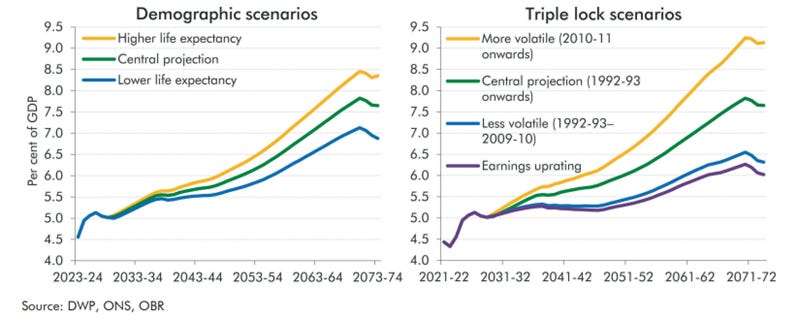

In recent years the policy has come under severe criticism with almost a critical mass of political consensus that something must be done about it. Following periods of elevated inflation and wage volatility, pension spending has risen faster than anticipated and the Office for Budget Responsibility (OBR) projects that, under certain demographic and indexation scenarios, state pension spending could approach 9% of GDP by the early 2070s particularly if life expectancy continues to increase (OBR, 2025). Figure 6 presents OBR charts for projected UK state pension spending across a range of scenarios for life expectancy and triple lock paths.

Figure 6 - Scenarios for state pension spending as a share of GDP (OBR, 2025).

These figures naturally prompt questions of sustainability. However, as has been made clear in this essay, a rising share of GDP devoted to state pensions simply means that a larger proportion of national output is being directed, via public transfer, to older citizens. It does not demonstrate financial insolvency but that choices must be made.

It is also important to retain perspective. Even after more than a decade of triple lock uprating, the UK state pension remains modest by international standards. Earnings replacement rates are still comparatively low, and the state pension age has been increased and is scheduled to rise further. It also remains just a basic income floor that aims to protect against poverty rather than guaranteeing affluence.

From a real economy perspective, the triple lock debate is the perfect example of how this problem space is too often confused. Can the UK allocate a somewhat larger share of its output to the elderly, and is it worth doing so to reduce poverty in old age? Sure, but it’s a distributional choice. That debate rarely extends to the broader distribution of retirement income. Rising dividend flows, interest payments, and rental incomes accruing to asset-rich retirees are seldom framed as sustainability concerns, even though they too represent claims on current output and could exert distributional pressure on younger or poorer households.

The focus instead settles on the comparatively modest public transfer, largely because of orthodox scepticism to socialised provision which rests on assumptions about the state and markets that are rarely made explicit or are based on shaky ideological foundations.

If adjustment is required, it need not take the form of cutting public pensions. It may instead involve redistributing private retirement income at the top, reforming property taxation, or reshaping pre-distribution in labour and housing markets so that younger generations are not disproportionately squeezed.

Viewed through this lens, the triple lock is not the central sustainability problem it is often portrayed as in the media and politics. It is one element in a much broader question about how real output is shared across age groups in a highly financialised and unequal economy. The debate should be conducted at that level.

The Policies to Build Real Retirement Security

This essay has spent time deliberately stressing the importance of correctly framing the problem of retirement provision and wider economic policy in macroeconomic real resource terms. Improving public understanding of society-level questions is a crucial catalyst to obtain better political discourse on these issues. Once this framing is achieved, the policy implications become much clearer.

If retirement ultimately represents a transfer of real output from workers to retirees, then policy must focus on the two levers identified above: the level and composition of that output, and the distribution of claims over it.

Of the second lever, perhaps the most important aspect is pre-distribution. The most robust way to ensure long-term retirement security is to guarantee a high level of productive participation across the economy. A permanent Job Guarantee (JG), operating as a macroeconomic stabiliser, would anchor wages and prices from cyclical and destabilising dynamics and ensure consistent full employment demand levels, all while expanding socially useful output. Rather than tolerating idle labour in downturns and speculative booms in upswings, such a framework would mobilise available capacity into care work, environmental restoration, community services, and local infrastructure.

The state will act as the marginal buyer of labour and employer of last resort, shifting the stabilisation mechanism from the money markets to the labour markets and mobilising the unemployed to produce socially additive value. This directly strengthens the real provisioning base required for an ageing society and significantly reduces the colossal real opportunity and social costs associated with unemployment.

Complementing this is a commitment to a structurally low policy rate, ideally a permanent Zero Interest Rate Policy (ZIRP) environment. This would reduce upward redistribution toward holders of financial wealth and diminish the regressive effects of risk-free interest income. In an ageing and unequal society, that mechanism disproportionately benefits wealthier retirees while increasing the real fiscal cost of public provision. The uncertainty of monetary policy settings over time is also a drag on firm investment and confidence over the long-term; another reason why patient capital formation is too often deprioritised.

Financial system and banking reform is equally central to complement ZIRP to prevent asset bubbles. Pension savings in the UK are deeply embedded within a financialised asset structure that often privileges speculation over productive investment. Bank Asset Regulation and Credit (BARC) policies can be redesigned to favour lending for real capital formation, sustainable and affordable housing supply, a green transition, and social infrastructure rather than leveraged property speculation or secondary market activity. Credit guidance, tighter regulation of bank capital requirements and reduced loan to value ratios represent a reassertion of the principle that banks exercise privileged credit-creation powers and therefore require commensurate public oversight.

Universal Basic Services (UBS) offer another structural layer of pre-distribution. If healthcare, public transport, education, childcare, and social care are collectively provided at high quality to all who need it, the real consumption burden out of income on both workers and retirees is reduced. Retirement security improves not only through income but through guaranteed access to essential services. Expanding social housing provision, particularly energy-efficient and accessible housing, similarly reduces lifetime living costs and mitigates the intergenerational housing transfer that currently characterises the UK model.

Alongside pre-distribution sits redistribution. The UK has witnessed a substantial rise in private pension wealth, dividend flows, and property-derived income accruing to older asset holders. These income streams represent claims on current output just as much as the state pension does. Yet they are rarely scrutinised within sustainability debates. A progressive consolidated tax framework applied to pension withdrawals, capital gains, rental income, and inheritances would complement the range of holistic policies designed to reduce intra-generational inequality. The triple lock is not the problem; distributional pressures arise less from the basic state pension than from highly concentrated private retirement income at the top of the distribution.

If part of the challenge of an ageing society is that a growing share of output must flow to retirees, then distribution within the retired population matters. Redistributing from asset-rich retirees to those reliant solely on the state pension can strengthen social cohesion without increasing the aggregate burden on workers and is an important part of this discussion. The political discomfort this raises should not obscure the economic logic that inequality within cohorts is as relevant as inequality between them.

These policies together reflect a broader reorientation. An economy that persistently channels credit toward unproductive asset inflation, rewards rent extraction, tolerates unemployment and underemployment, and measures success primarily through aggregate GDP growth is poorly designed. It will fail to manage demographic transition and an ecologically constrained future. A sustainable retirement system requires an economy oriented toward human need rather than speculative return and it requires democratic control over macroeconomic policy levers. Deference to financial markets or a tolerance for the current democratic deficit in central bank stabilisation policymaking only hamper long term progress.

The sustainability of retirement provision is therefore inseparable from the sustainability of the entire economic model. Climate instability, ecological degradation, fragile global supply chains, and geopolitical fragmentation pose real threats to future provisioning capacity. Ensuring food security, energy resilience, and domestic productive capability is not peripheral to pension policy, it is foundational. An ageing population cannot be supported by financial assets if the real systems those assets claim upon are compromised.

To receive new posts and support my work, consider becoming a free or paid subscriber.

Conclusion

The central argument of this essay is straightforward. I’ve attempted to communicate the need for a wholesale shift in how we understand and frame questions around retirement provision from one of financial sustainability to one of holistic real resource availability. Every pension system, public or private, is a mechanism for transferring part of current output from workers to retirees. The institutional design does not alter that reality in aggregate; what matters is whether the economy produces enough of the right things, in the right proportions, and whether access to that production is distributed in a socially legitimate and ecologically sustainable way. Markets and private capital allocation alone are insufficient mechanisms of achieving this wider public purpose.

The triple lock is not the fiscal time bomb we are consistently warned it is. Rising pension spending as a share of GDP is not evidence of insolvency; interest rates are policy variables, not market determined constraints; financial crowding out is only applicable at the real level, not a binding nominal constraint for a currency-issuing state; and the genuine constraints are labour capacity, ecological boundaries, productive investment, and distributional structure.

If we continue to frame the pension debate through the language of budget fiscal rules and affordability fears, we will design policy for a problem that does not exist while neglecting the problems that do. If instead we re-centre the discussion on real resources, sectoral composition, and democratic allocation of economic power, different priorities emerge.

An economy committed to full employment, financial stability, equitable distribution, ecological sustainability, and universal access to essential services can support an ageing population without intergenerational conflict. It can ensure that retirees live with dignity while younger generations inherit productive capacity rather than misleading debt myths and inflated asset bubbles.

Retirement provision is not an accounting challenge. It is a societal choice. It forces us to ask what we produce, who we produce it for, and who commands its fruits. If we are willing to confront those questions honestly and redesign our macroeconomic architecture accordingly, then the future of pensions will be durable and built on socially legitimate and sustainable foundations.

References

C-SPAN. (2005, March 2). User Clip: Greenspan: “There is nothing to prevent the government from creating as much money as it wants.”. CSPAN. USA. Retrieved from https://www.c-span.org/clip/house-committee/user-clip-greenspan-there-is-nothing-to-prevent-the-government-from-creating-as-much-money-as-it-wants/5028493

House of Commons Library. (2024, December). Pensions: international comparisons. House of Commons. London. Retrieved from https://commonslibrary.parliament.uk/research-briefings/sn00290/#:~:text=The%20UK%20devotes%20a%20smaller,than%20most%20other%20advanced%20economies

IFS. (2025, October 21). What are the effects of the ‘triple lock’ and how could it be reformed? Institute for Fiscal Studies. UK. Retrieved from https://ifs.org.uk/articles/what-are-effects-triple-lock-and-how-could-it-be-reformed#:~:text=lock%E2%80%99%3A%20the%20highest%20of%20CPI,amount%20very%20close%20to%20this

Money Week. (2025). UK state pension is least generous in the G7 – how do other rich countries compare? Money Week. Retrieved from https://moneyweek.com/personal-finance/state-pensions/uk-state-pension-compared-g7-countries#:~:text=UK%20retirees%20receive%20just%20over,and%20Italy%20%2876

OBR. (2025). Fiscal Risks and Sustainability. London: Office for Budget Responsibility. Retrieved from https://obr.uk/docs/dlm\_uploads/Fiscal-risks-and-sustainability-report-July-2025.pdf

ONS. (2019). Living longer and old-age dependency – what does the future hold? Office for National Statistics. UK Government. Retrieved from https://www.ons.gov.uk/peoplepopulationandcommunity/birthsdeathsandmarriages/ageing/articles/livinglongerandoldagedependencywhatdoesthefuturehold/2019-06-24#:~:text=,aged%2065%20years%20or%20over

ONS. (2025, January). Office for National Statistics.

The Global Economy.com. (2024). The Global Economy.com. Retrieved from https://www.theglobaleconomy.com/United-Kingdom/Age\_dependency\_ratio/

UK Gov. (2024). Pension fund investment and the UK economy. UK Government, Department for Work and Pensions. London: UK Government. Retrieved from https://www.gov.uk/government/publications/pension-fund-investment-and-the-uk-economy/pension-fund-investment-and-the-uk-economy

Wray, R., & Nersisyan, Y. (2023). Demographics, the economy and the environment: An MMT approach. Real-world Economics Review(106). Retrieved from https://www.paecon.net/PAEReview/issue106/Wray\_Nersisyan106.pdf#:~:text=WKDW%20WKHUH%C2%B6V%20QRWKLQJ%20WR%20SUHYHQW,be%20enough%20real%20output%20for